Every counter-fraud operation runs on data. Detection models are fed data to identify suspicious patterns. Investigators draw on data to build their cases. Management information reports data to leadership as the evidence base for operational decisions. The question most counter-fraud teams do not spend enough time on is the quality of that data. When what is going into the operation is incomplete, inaccurate, or out of date, the detection outputs become less reliable, the investigation workload grows unnecessarily, and the MI that reaches the Head of Fraud tells a story that does not fully reflect what is actually happening.

Anyone who has sat in a quarterly MI review and questioned a savings figure, or tried to reconcile a referral count that does not match the closed case tally, has already encountered this problem in practice. The Office for Statistics Regulation’s 2025 review of fraud and computer misuse statistics for England and Wales flagged data quality as a consistent concern across institutions responsible for fraud reporting, identifying specific issues around completeness and consistency. That review is about national crime statistics rather than insurance operations specifically, but the structural problem it describes, data that is not complete, accurate, and timely producing unreliable outputs, maps directly onto what happens inside SIU teams when case data is captured inconsistently and MI is compiled from whatever the system happens to contain.

Key Takeaways

- Counter-fraud operations depend heavily on data quality, affecting detection, investigation, and management reporting.

- Data quality in insurance counter-fraud involves completeness, accuracy, and timeliness of information collected at all operational layers.

- Poor data management leads to unreliable detection outcomes, higher false positive and negative rates, and inefficient resource allocation.

- Accurate management information (MI) supports better decisions on resource allocation and strategy in fraud operations.

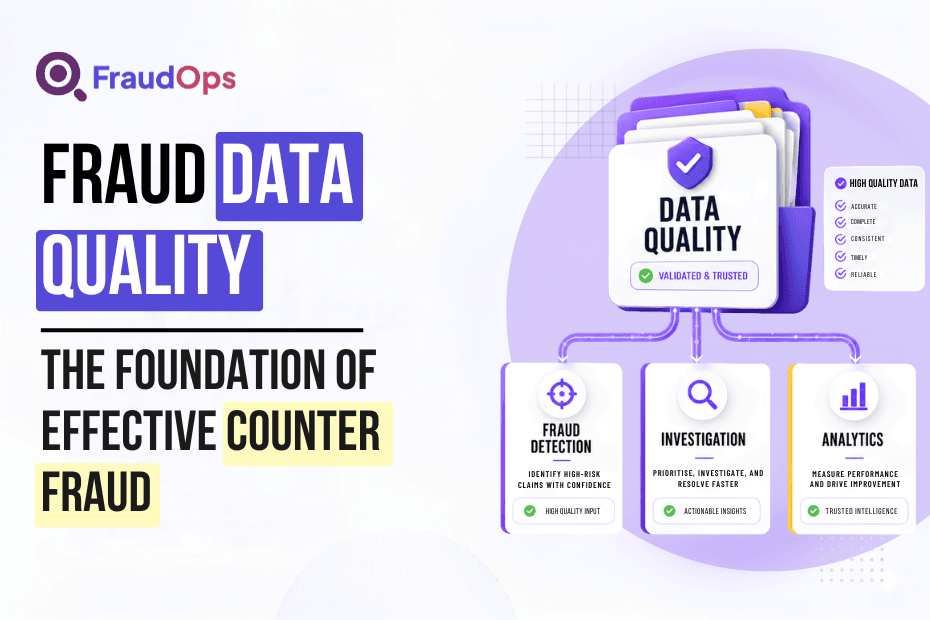

- FraudOps enhances data quality by structuring case data from the point of referral, ensuring consistency and reliability throughout the investigation pipeline.

What Fraud Data Quality Means in an Insurance Counter-Fraud Context

The Government’s Fraud Prevention Savings Framework, published in May 2026, offers a definition developed for public sector fraud prevention that translates cleanly into the insurance context: data quality covers completeness, accuracy, and timeliness. A complete dataset captures all the cases and entities it should, without gaps caused by disconnected systems or records that were never structured consistently. An accurate dataset reflects what actually happened, with the right details recorded against the right case and the right outcome. A timely dataset is current, updated when new information arrives rather than at a quarterly reporting cycle. These three dimensions are not specific to public sector fraud. They describe the same problem any counter-fraud team faces when the data it generates is not fit for the purposes it is being put to.

In insurance counter-fraud specifically, the concept of fraud data quality runs across several connected layers. It covers the accuracy of the referral record that arrives from claims handling. It covers the completeness of the case record investigators build as they work through a referral. It covers the integrity of the intelligence records that feed into future detection and triage decisions. And it covers the reliability of the MI that comes out at the other end and informs decisions about where the operation should focus its resources. Each of those layers depends on the one before it, which is why gaps at the referral stage tend to produce problems all the way through to the reporting stage.

Why the Quality of Insurance Fraud Intelligence Data Shapes Detection Outcomes

The argument for treating insurance fraud intelligence data as a quality-controlled asset rather than a passive record is most visible in how shared industry databases work. Most UK insurers rely on shared intelligence platforms, industry fraud databases, and vendor-supplied detection tools rather than building and maintaining bespoke detection models on their own case history alone. The value any individual insurer gets from those shared resources depends directly on what the collective membership contributes to them. An insurer contributing well-structured, accurately classified case outcomes generates intelligence that improves detection across the market and feeds back into its own future referrals. An insurer contributing incomplete or loosely classified records does the opposite, and the effect accumulates across every case that passes through an undisciplined data process.

Cifas Fraudscape 2026 reported that over 444,000 cases were filed to the National Fraud Database in 2025, a record number continuing the upward trend seen in 2024. The NFD spans multiple sectors, but the quality principle it illustrates applies directly to insurance-specific databases: shared intelligence is only as useful as the quality of what goes into it, and inconsistent data from one contributor reduces the reliability of outputs for everyone who draws on the same resource.

The Counter Fraud Data Management Problem Most Teams Are Not Tracking

The operational consequences of poor counter fraud data management tend to build gradually rather than announce themselves in a single failure. An investigation queue grows because referrals are arriving without the supporting context investigators need to proceed efficiently. Triage decisions are made on incomplete information, which produces either a higher false positive rate consuming investigator time on cases that will not convert, or a higher false negative rate allowing fraud through that the available data should have flagged. Cases that should connect to an organised fraud network stay isolated because the data that would link them was never recorded in a consistent format.

The ABI’s 2024 fraud data recorded £1.16 billion in fraudulent general insurance claims across 98,400 detected cases. The word “detected” carries significant weight in that figure. The fraud counter-fraud teams catch is the fraud the data they hold allows them to find. The portion that goes undetected is not visible in the numbers, but the quality of the data available for detection is a direct factor in where that boundary sits between detected and missed.

For UK counter-fraud teams managing growing referral volumes with broadly flat investigation capacity, the consequence of poor data management compounds with scale. More time goes to manual data correction and reconciliation before a case can progress. More cases sit incomplete in the investigation queue. More management reports are compiled from data that was never consistently structured, producing MI that is difficult to act on with any confidence in what it is actually measuring.

Fraud MI Data Accuracy and What It Means for Operational Decisions

The point in the process where fraud MI data accuracy has the most direct impact on a counter-fraud operation is at the management level, where reporting is used to make resource and strategy decisions. A Head of Fraud working from MI that accurately reflects the investigation pipeline, the conversion rate by fraud type, and the savings produced by each referral source has a solid basis for deciding where to direct capacity and what adjustments to make to the detection or triage process.

The same MI, produced from case data that was inconsistently captured or incompletely recorded, gives a distorted picture. Conversion rates look lower than they are because some confirmed fraud savings were never recorded against the originating referral. Cycle time metrics are misleading because cases that were never formally closed still appear as open in the pipeline. Referral quality scores by source are unreliable because the classification applied at triage was not consistently applied across the team. Each of those distortions is individually manageable, but together they make the MI report a less reliable tool for the decisions it is supposed to support.

A practical version of this problem that most SIU teams will recognise is outcome recording. When investigators use a free-text field to close a case rather than selecting from a standardised outcome classification, the MI dashboard cannot reliably distinguish a confirmed fraud saving from a claim settled commercially to avoid a protracted dispute, or a case withdrawn because the claimant dropped the claim after investigation began. All three outcomes look identical in the data. The savings figure is wrong, the conversion rate is wrong, and the management decision about where to focus investigation resource is being made on a number that does not mean what it appears to mean.

How FraudOps Supports Data Quality Across the Investigation Pipeline

FraudOps structures case data from the point of referral intake, which means the data quality discipline is built into the workflow rather than applied retrospectively. Cases are created with a consistent structure regardless of the referral source. Fraud type classification is applied at intake and updated as the investigation develops, with every change recorded in the audit trail. Investigation outcomes are captured against the originating referral so the connection between referral source and savings outcome is maintained across the full pipeline rather than lost at case closure.

The MI layer draws on that structured case data in real time, so the reporting available to the Head of Fraud reflects the actual state of the investigation pipeline rather than a manually compiled summary that may be weeks behind operational reality. Every automated action within the platform, including AI-generated document summaries and automated data lookups, is recorded and auditable, which means the data generated by automation meets the same quality standard as data entered directly by investigators.

The Bottom Line

The performance of a counter-fraud operation is determined by the quality of the data it runs on. Detection models identify what the data allows them to find. Investigation decisions are only as reliable as the case record they draw on. Management information communicates what the data it is built from actually captures.

For counter-fraud data management across UK insurance teams, the practical priority is not generating more data. It is improving the reliability of what the operation is already producing: consistent fraud type classification at intake, complete case records at closure, investigation outcomes recorded against referral source, and MI reporting drawn from structured case data rather than manual compilation.

The fraud that costs UK insurers over a billion pounds a year, as the ABI’s 2024 figures confirm, is being detected and investigated on data that most counter-fraud operations have not yet optimised for quality. The teams getting the best outcomes are treating data quality as a continuous operational discipline rather than a technical problem to be solved once and left alone.